I was wondering today whether my strategy of paying off my home loan early instead of investing is indeed the best. You know, pay home loan or invest? There are so many things to consider and I sometimes relook at my reasoning to see if it is still sound. I’m actually feeling a little uncertain now but here is my thought process and considerations and it would be great to hear your views in the comments section.

The synopsis

The problem is simple, pay home loan or invest. So do I pay off the bond and be debt free, or do I keep paying debt and invest at the same time?

For this example we will look at a home loan of R1,400,000 paid monthly over 20 years at an interest rate of 10.5%. Then, along with paying off the bond we have R2,500 per month extra to either pay into the bond or to invest. These figures are just examples to help with the calculations.

This post will look at the calculations as well as some of the other considerations to look at. (See how to calculate interest using the Excel formula here)

Pay off home loan or invest?

Update Jan 2021

Just to share an update – I have now fully paid off my home loan and and 100% debt free. And, I’ve written a step-by-step guide on how to get out of debt, if you’re interested.

Introducing the calculation

This first example shows that when the interest rate of the home loan is the same as the growth on the investment, it makes no difference where you put your money. You can put it in the bond or invest it and it will grow at the same rate. (See the flaws and assumptions section)

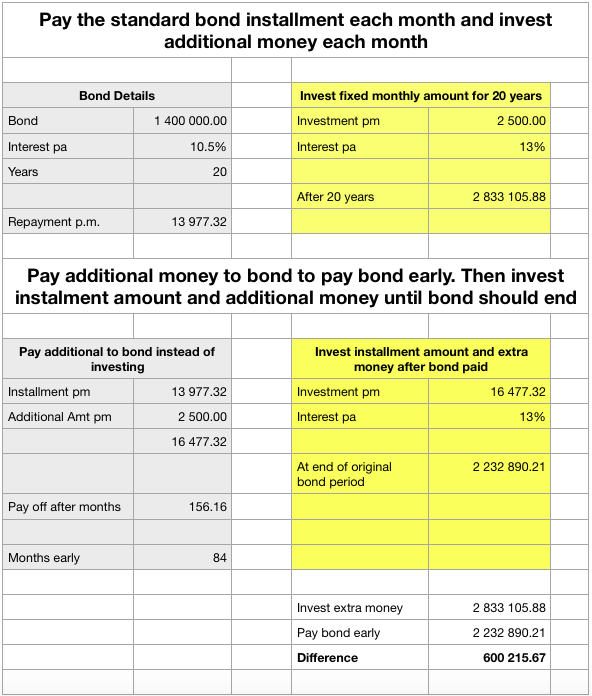

In the example below, the top left grey section shows the standard bond payment. In this case the bond of R1,400,000 will have a monthly instalment of R13,977.32.

The top right yellow box shows an investment of R2,500 per month with a fixed growth of 10.5% also over a 20 year period. You will see that after 20 years you will have a fully paid off property as well as investments worth just over 2-million.

Now look at the scenario in the bottom section where we pay the additional money we have straight into the bond and we pay the loan off 84 months early. Then, once the loan is paid we take the full amount that we were paying as the instalment as well as the additional money we have and we invest it for the remaining period. So we invest R16,477.32 monthly for the remaining 84 months.

You will see that if the home loan interest rate and the investment growth are the same, it makes no difference. The real difference lies in the interest rate!

Try out the Home Loan Calculator here

The calculations with different interest rates

In this example the only change is that the investment growth is set to 13% (in the previous image you will see it was 10.5% which is the same as the home loan interest rate)

Now you will see that it is definitely better to invest money at a higher interest rate instead of paying the loan off early. And obviously the bigger the difference between the home loan interest rate and the investment growth rate, the bigger the final monetary difference!

So, if we increase the investment growth rate to 15% then the difference is R 1,326,026.40 which is starting to sound like a serious amount of money!

If you’re interested in doing the calculations yourself, have a look at this Udemy Course which will help you understand all the home loan calculations needed.

Flaws and assumptions

Looking at this it really makes sense to invest extra money you have instead of paying off debt. However, there are some flaws in the calculations:

Investment growth not guaranteed

It’s very easy to add higher investment returns in a spreadsheet but unfortunately it’s impossible to predict or guarantee investment growth. One can look at funds and use the average growth rate, but as markets go up ad down things change.

You may not always have the spare money to invest

We’re assuming that you will have extra money each and every month for 20 years. This may not be so as life sometimes throws curveballs and its impossible to predict.

Fees & Tax not taken into account

The investment choice will obviously have fees and taxes to take into account which is just too complex for right now. It probably won’t have a huge impact on the final figures but it is something to consider.

Do the calculations yourself

It’s all fair and well looking at a random example but wouldn’t it be better to learn to do these calculations yourself?

Why am I paying home loan off early instead of investing?

It really would seem that it’s better to invest the extra money I have from right now as the longer money is invested, the more the growth compounds. However, it’s not as straight-forward as that and there are some less concrete considerations too. Here are some reasons to be paying extra on your home loan:

Peace of mind

A really huge consideration for me is simply the peace of mind knowing that I am debt-free. Once the house is paid off there is literally no more debt and I don’t plan to ever have debt again. This peace of mind is valuable to me as it means that I don’t have this noose of debt around my neck! See my post on how to invest in freedom by paying off your home loan.

The goal is to travel

My partner and I have decided that traveling is a high priority for us in life and that we need to enjoy the experiences while we can. See how I budget for travel. Paying off the home loan will enable us to fulfil this. The current plan is to pay off the loan by the end of 2020 and then sometime after that we will pack up, rent out the house and use that income to support us for a year of travel. It won’t be luxurious and we will lose out on a year of investing, but the life experience will be invaluable to use!

Escape the rat race

Killing the debt is our first step to escaping the rat race of boring 9 – 5 jobs. Once our year of travel is over we will need to figure out how we want to shape our lives. Having a fully paid off property will give us much more leeway and space to make decisions.

Investing extra money each month for 20 yers certainly sounds like the right thing to do but we just don’t know what the future will bring. Something that is completely impossible to calculate is the investment made into our own lives. The opportunities that may reveal themselves and the opportunities that we create ourselves.

Working a stable job is just that; it’s stable. But allowing yourself time and space to explore other things is again invaluable.

Guaranteed growth

South Africa (as many countries) is currently experiencing some financial instability in that markets are dropping and rating agencies have downgraded us. This reflects in investments which have taken a knock in the short-term and although markets will inevitably bounce back and grow to newer heights, we need the short-term stability of guaranteed growth to enable us to reach our goal.

Tax free & no admin fees

The growth on money in your home loan (or any loan) is tax free. This may not be relevant to many people but it is useful to know. Also, your bond already incurs monthly fees which you are paying and by investing more money in the account no further charges are levied.

In closing, pay home loan or invest?

While investing money is obviously the more profitable outcome you need to look at life holistically and decide what’s going to bring you happiness and how you can create new opportunities for yourself. There is unfortunately no right or wrong answer when looking at very long term plans as we simply cannot predict the future. Absolutely anything could happen! So the best thing is to have a plan that seems reasonable and sound to you and that will help you reach your goals and bring some element of joy to you.

I have spare cash now so I would rather pay the debt while I can. This is why I’m paying my home loan off early instead of investing. What do you think? Is paying extra on your home loan worth it? Would you rather pay home loan or invest?

Home loan calculator

If you are looking at how to pay off your bond, check out the Home Loan Calculator which will give you a breakdown of monthly payments and the interest and principle amount. You can also see how much interest you are paying initially and why it makes so much sense to pay off your bond!

Pay home loan or invest: UPDATE – MAY 2019

After many comments and discussions about this post I decided to a) clarify something and b) rethink my strategy a little.

a) To Clarify

So firstly, it’s important for me to clarify that even though I have been putting away all my extra cash into my home-loan, I do have a company provident fund that I contribute to and I do have some pre-existing investments. So I have not given up on investments. When deciding whether to pay off home loan or invest, I am focusing on paying the debt but so still have investments.

b) A slight change to my strategy

I have however changed my strategy slightly as from the beginning of the year. I calculated the exact amount that I need to pay into my loan in order to pay it off by the end of 2020. Once that amount is paid I am investing all the rest into either existing investments or my new ETF investment. So I am really paying off my home loan early AND investing at the same time.

Hear me chat to Andy Hill on why and how I paid my home loan

Mortgage free in South Africa in less than 5 years…